As online spending continues to grow, so does the prevalence of disputes and chargebacks. Global chargeback volumes are projected to reach 377 million transactions by 2026, a 42% increase from 2023. Chargeback disputes arise from true fraud, first-party fraud, or merchant error, and can be challenging to predict and prevent, often disrupting business operations and compromising profitability. To effectively minimize these impacts, businesses need to proactively analyze the underlying causes of disputes and develop strategies to mitigate their effects on the bottom line.

Q4 2024 DIGITAL TRUST INDEX

Decoding Dispute Trends

Powered by FIBR, the Fraud Industry Benchmarking Resource

Current State of Disputes

Disputes and Chargebacks on the Rise in 2024

Data from the Sift Global Network indicates a significant increase in the average dispute rate, which rose by 78% year-over-year in Q3 2024. Due to a higher percentage of transactions being contested during this time, it could hint at increased dispute rates and chargebacks during the holiday season and into 2025.

There’s also evidence that more disputes are resulting in chargebacks in 2024. After a 14% decrease in the average chargeback rate throughout 2023, the first three quarters of 2024 saw an 8% increase across the Sift network. Fraudsters are evolving their methods to commit more fraud, and economic pressures continue to prompt more consumers to successfully dispute legitimate charges.

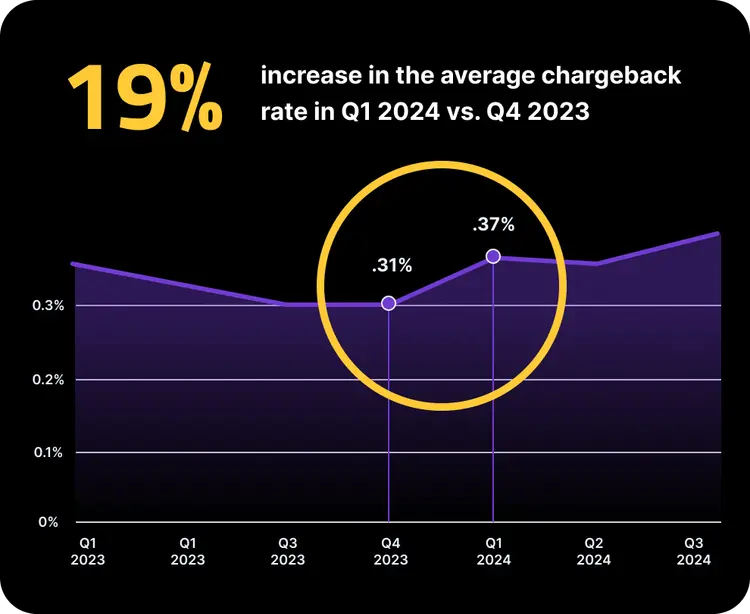

Between Q4 2023 and Q1 2024, the average chargeback rate increased by 19%, correlating with the holiday season’s surge in spending and subsequent chargebacks. Heightened transaction volumes and consumer spending during this period creates more opportunities for both true fraud and first-party fraud.

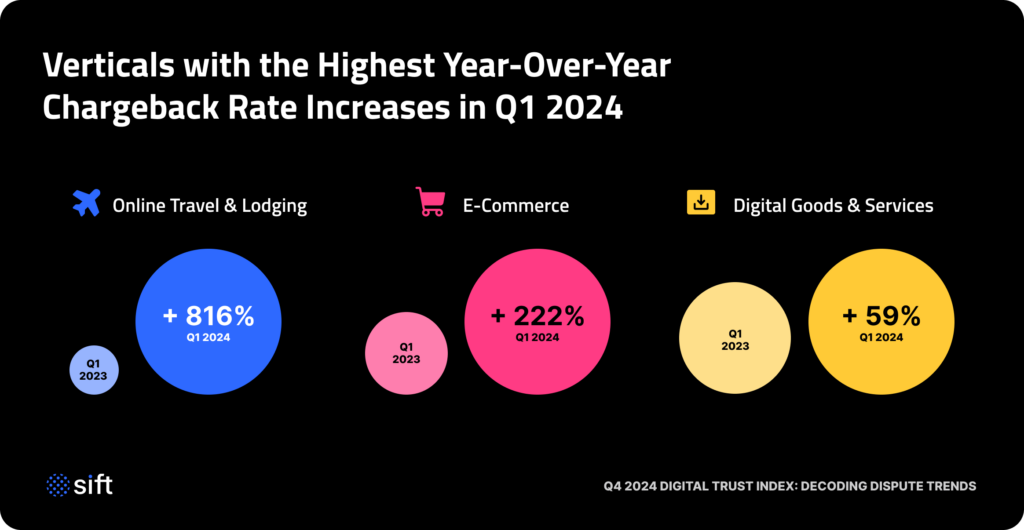

Chargeback Rates Spike Across Major Sectors

Certain sectors experienced the highest increases in chargeback rates year-over-year in Q1 2024. Online travel and lodging saw an astounding 816% increase. The post-pandemic travel boom is likely playing a substantial role in this surge, with consumers more frequently disputing charges for cancellations, delays, and dissatisfaction with services. Likewise, the e-commerce industry experienced a 222% increase in chargeback rates. With more consumers shopping online, disputes stemming from consumer dissatisfaction, delivery issues, and first-party fraud are common. Digital goods and services saw a 59% increase in chargeback rates, likely due to first-party fraud, limited manual review time, and the lack of shipping address verification.

See the Full Report

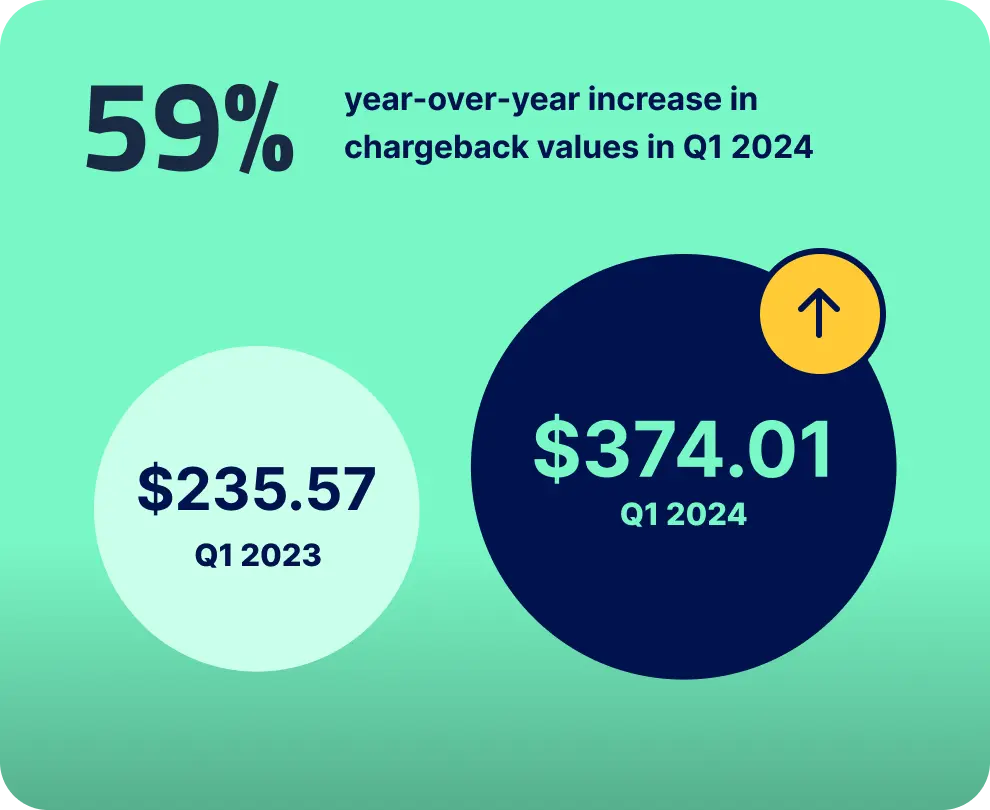

Chargeback Values Surge in 2024

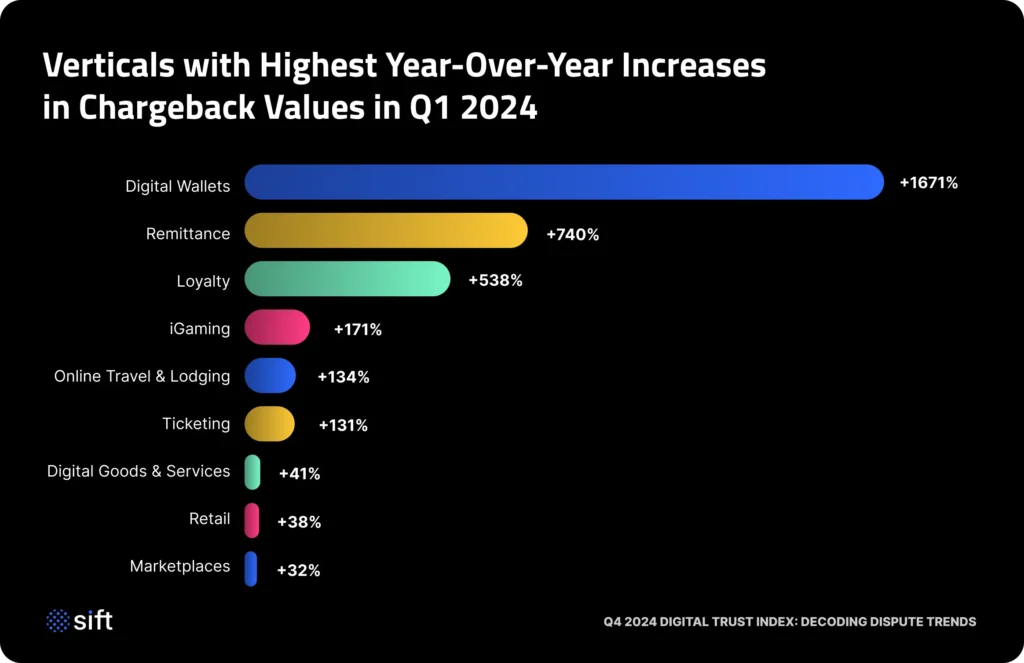

Chargeback values surged significantly during this year’s chargeback season, jumping 59% year-over-year in the first quarter of 2024. The average chargeback value rose from $235.57 in Q1 2023 to $374.01 in Q1 2024. Businesses in the fintech sector, particularly digital wallets, remittance services, and loyalty programs have experienced the most significant increases in chargeback values—reflecting a growing trend of fraudsters targeting emerging markets. The steady rise in dispute and chargeback rates across industries, along with the sharp increase in chargeback values, indicates that fraud operations will likely become more costly in 2025.

Consumer-Driven Dispute Insights

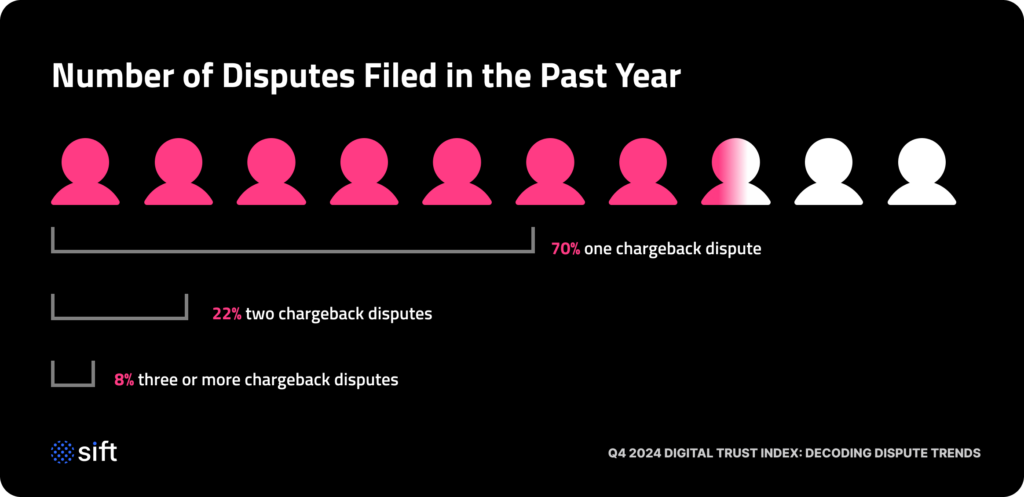

Nearly three-quarters of consumers surveyed* by Sift reported that they disputed a purchase in the past year. Of those consumers, 70% filed one chargeback dispute, indicating that most are not habitual disputers but may have encountered a single issue that prompted their action. Meanwhile, 22% of consumers filed two chargeback disputes, suggesting undetected unauthorized transactions or misuse of the dispute process. The remaining 8% filed three or more disputes, representing a minority that includes habitual first-party fraudsters or multiple compromised payment credentials.

Chargeback Rates Spike Across Major Sectors

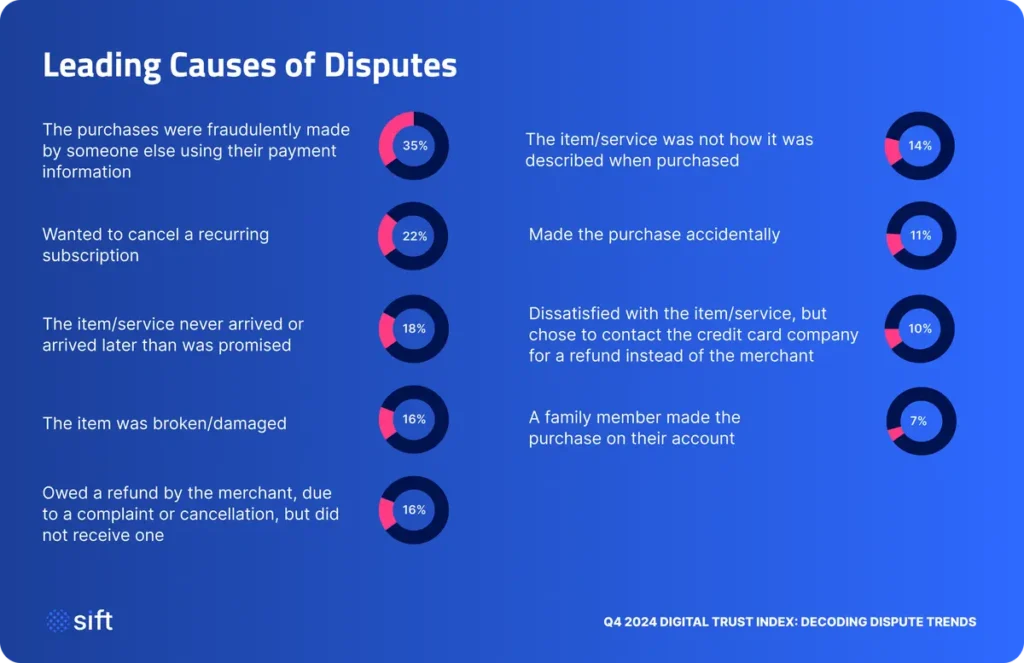

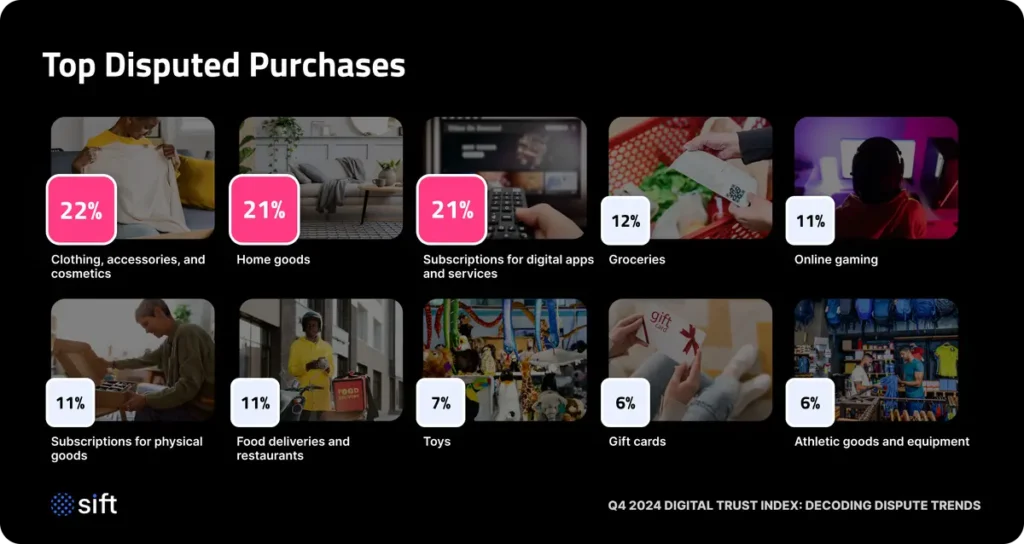

About one-third of disputes were due to true fraud, down from 44% in 2023, indicating a rise in first-party fraud. The data suggests more consumers are exploiting the chargeback process to dispute legitimate transactions. Consumers’ reasons for filing these disputes can vary, ranging from wanting to get out of a recurring subscription, to being dissatisfied with their purchase. Consumers most frequently dispute items such as clothing, accessories & cosmetics, home goods, and subscriptions for digital apps & services. These disputes often stem from issues such as fit, quality, buyer’s remorse, delivery problems, and difficulties with subscription cancellations.

More Consumers Turn to First-Party Fraud

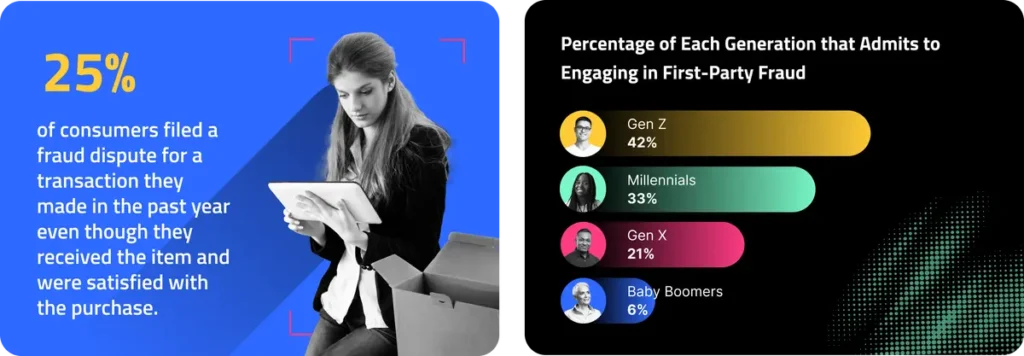

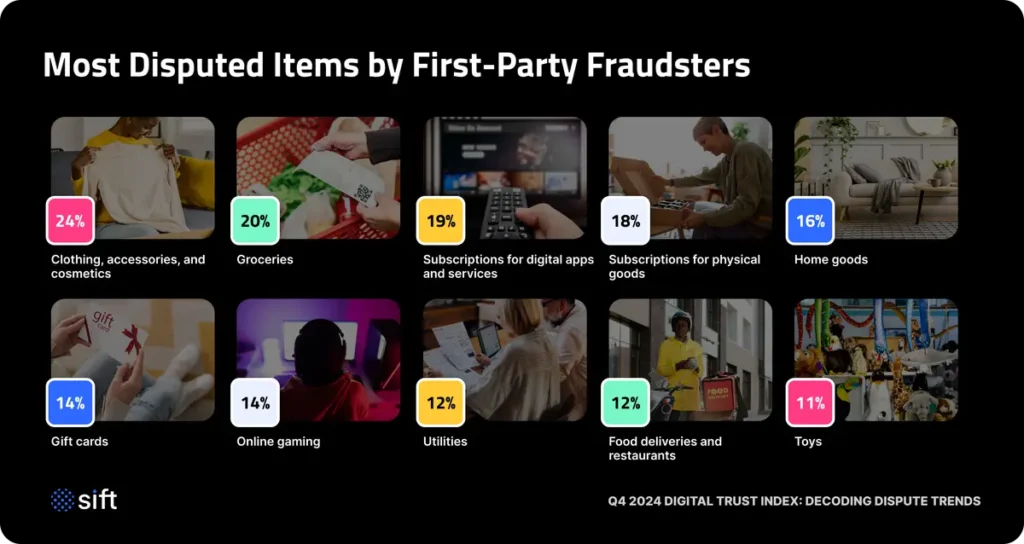

Over the past year, a quarter of consumers admitted to first-party fraud, filing fraud disputes despite being satisfied with their purchases. Many consumers are filing disputes for illegitimate reasons, either with malicious intent, such as wanting their money back, or due to lack of education about return policies. Disputes were common for clothing, accessories, cosmetics, groceries, and subscriptions. Compared to all dispute filers, first-party fraudsters were more likely to dispute necessities like groceries, accounting for the second most disputed item. One study found that 70% of consumers struggle with grocery affordability, marking the third consecutive year of rising costs for households and highlighting the financial strain on consumers.

Younger consumers are significantly more likely to commit first-party fraud, filing false disputes for transactions they made and were satisfied with. This tendency decreases with age, suggesting that older generations are less prone to the behavior. The generational divide may stem from several factors: younger individuals might not realize their actions constitute fraud, using chargebacks to sidestep strict return policies, or they may intentionally exploit the system to reclaim their money, sometimes driven by dissatisfaction with a business.

The Democratization of Fraudulent Disputes

Economic stress has led many consumers to find creative ways to save money, including participating in first-party fraud. The democratization of fraud has lowered the barrier to entry, with modern scammers using social media to sell tips and tactics, making fraudulent activity more accessible. Fraud tools and technology are available on the deep web, which offers on-demand Fraud-as-a-Service (FaaS) tools and services that anyone can purchase to commit fraud. On messaging apps like Telegram, fraudsters share tips for exploiting retailer return policies, leading to more widespread return fraud and deeper financial losses for merchants.

With a significant 27% of consumers encountering online content offering “hacks” to get refunds despite being satisfied with their purchase, it’s easier now than ever for shoppers to take advantage of refund and dispute policies. Of these consumers, millennials and Gen Z were more likely than Generation X and baby boomers to encounter online content on how to hack the refund process. Similar data shows the younger the consumer, the more likely they are to engage in first-party fraud. The evidence demonstrates that increased exposure to this type of discourse can directly influence behavior.

Payment Fraud Causes a Chain Reaction of Abuse

Consumers who filed a dispute due to true fraud often faced additional fraudulent activity. Data shows that 28% of these consumers were subsequently victims of additional online fraud. Of these consumers, 61% experienced additional payment fraud, 44% received increased spam or scam messages, and 30% suffered account takeovers. In many cases, consumers didn’t notice or weren’t alerted of suspicious activity in time to cancel their cards or change their passwords to prevent further harm.

The Opportunity Cost of Unauthorized Transactions

Although the majority of fraud-related chargebacks stem from first-party fraud, there are considerable costs associated with not protecting trusted consumers from becoming victims of payment fraud. Unauthorized purchases made on a brand’s website or app can significantly impact consumer loyalty.

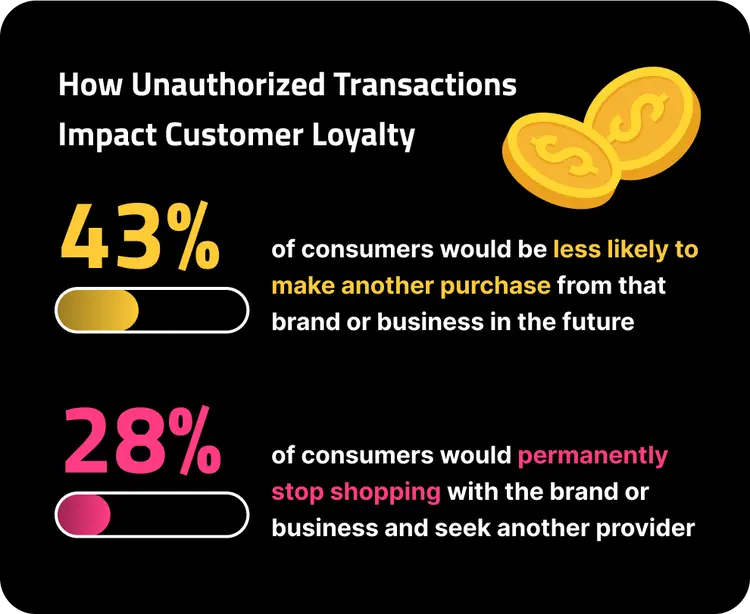

Survey results show that 43% of consumers would be less likely to make a purchase from a brand if they experienced an unauthorized transaction on that brand’s website or app. Another 28% of consumers would permanently stop shopping with the brand and seek out another business. Many consumers hold brands responsible for payment fraud on their sites, leading to lost trust and lifetime value (LTV). It also negatively affects customer acquisition costs and growth opportunities, forcing brands to spend resources on reactive measures instead of improving the customer experience or expanding their customer base.

Fraud-related chargebacks continue to rise overall, despite a slight reprieve in 2023, driving organizations across industry lines to dive deeper into a holistic fraud prevention strategy.

Alexander Hall

Trust and Safety Architect at Sift

Mitigating Chargebacks with AI-Powered Fraud Protection

Businesses must be prepared for the upcoming 2025 chargeback season by understanding the true cost and consequences of chargebacks. With the anticipated increase in chargeback rates and values following the holiday shopping period, implementing best practices for dispute management is essential.

Fraud and risk teams should focus on preventing first-party fraud through clear cancellation and return policies, leveraging Visa CE 3.0 to defend against illegitimate chargebacks, preparing for the evolved Visa Acquirer Monitoring Program (VAMP), and using advanced solutions to prevent fraud across the user journey. By prioritizing winnable cases, efficiently gathering compelling evidence, and submitting quick responses, businesses can improve their chargeback win rates and minimize financial losses.

Leveraging Sift’s AI-powered fraud solutions provides a proactive approach to mitigating the risk of chargebacks and other fraudulent activities. Sift analyzes transaction patterns in real time to identify potential fraud and automate the dispute management processes, enhancing overall business operations. By integrating comprehensive fraud prevention and dispute management solutions, companies can stay ahead of evolving fraud tactics, protect their revenue, and secure the customer journey.

*On behalf of Sift, Researchscape International polled 1,156 adults (aged 18+) across the United States via online survey in October 2024.

What’s New at Sift

Drive Your Business Forward with FIBR

Compare your own data against Sift benchmarks with FIBR, the first Fraud Industry Benchmarking Resource of its kind delivering crucial fraud insights to businesses across verticals and regions.