As digital commerce grows, the frequency and financial impact of disputes and chargebacks is expanding. Global chargeback volume is projected to reach 324 million transactions by 2028, up 24% from 2025, driven largely by the expansion of card-not-present (CNP) payments, which now make up 63% of merchants’ transactions.

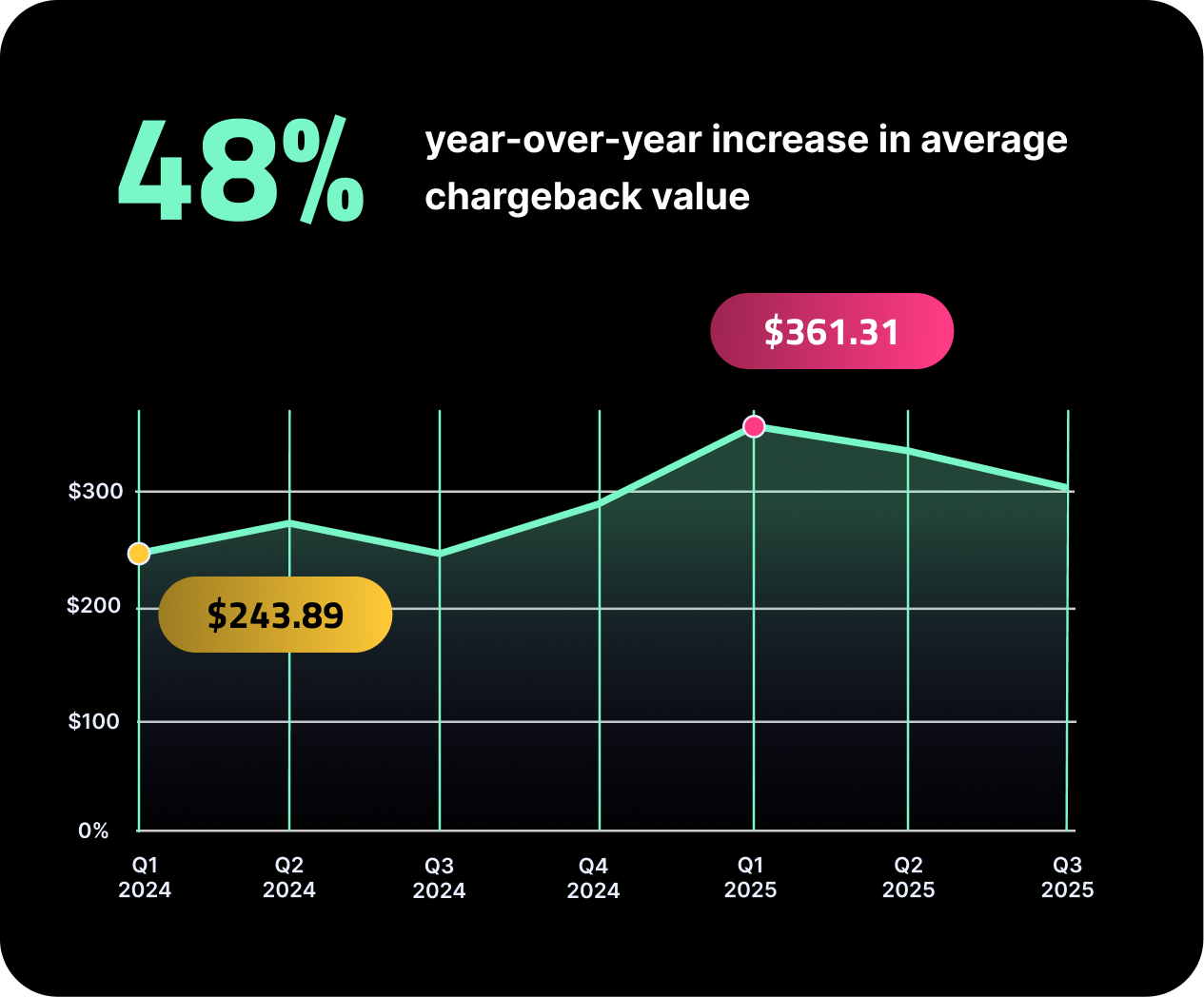

The cost burden is growing just as quickly. Worldwide chargeback losses are expected to climb from $33.79 billion in 2025 to $41.69 billion in 2028, while first-party and third-party fraud now account for roughly 45% of merchant dispute volume. With U.S. merchants losing an estimated $4.61 for every $1 in chargebacks, understanding the root causes of disputes—and strengthening prevention strategies—is becoming essential to protecting both revenue and customer trust.