Fast-growing platforms face a relentless onslaught of payment fraud. The stakes are high: according to MasterCard, global online payment fraud losses are expected to exceed $343 billion from 2024 to 2027. Every fraudulent chargeback or false decline hits the bottom line and erodes customer trust. To tackle this threat, product and engineering leaders must ask a pivotal question: do we build our own in-house fraud prevention platform, or do we leverage a third-party solution like Sift?

Businesses need a strategic framework for evaluating the build-or-buy decision when it comes to payment protection, and prioritize blending strategic insight with technical depth.

The Scale and Complexity of Payment Fraud

Scaling payment fraud is complex and constantly evolving. Fraudsters exploit any weakness. I’ve seen scammers use stolen credit cards to place orders and run illicit schemes reselling discounted services or goods. That leaves the platform reimbursing victims for fraudulent charges (as well as eating chargeback fees) when the fraud is discovered.

Many companies initially rely on manual reviews and basic rules, but those approaches can’t keep pace with clever attackers. Rules-based systems need continual updates to fend off new fraud patterns, consuming valuable time and resources. Despite these efforts, losses mount quickly—fraud scales with growth and can rapidly threaten a platform’s profitability and reputation.

Staying Ahead of Evolving Fraud Tactics

Sophisticated fraud rings adapt rapidly, even using advanced technology to outmaneuver defenses. Some are even leveraging machine learning themselves to probe and reverse-engineer fraud controls. If your defenses are slow to adapt, attackers will find loopholes. This puts the onus on companies to innovate quickly and stay agile in their fraud-fighting tactics.

Machine learning is a cornerstone of modern fraud prevention because it can detect subtle, emerging patterns. Sift’s AI-powered models, for example, continuously gather new intelligence from across our customer network, updating them in real time. A purpose-built system can flag novel fraud signals instantly, whereas an in-house tool might lag if it’s not constantly tuned.

As fraudsters deploy AI and new strategies, we need to “fight fire with fire” by leveraging equally sophisticated technology. Staying on top, if not ahead, of attackers requires a level of innovation and agility that can strain a typical in-house team, unless fraud prevention is one of the company’s core competencies or a revenue-generating product.

Building In-House: Resource, Talent, and Total Cost of Ownership

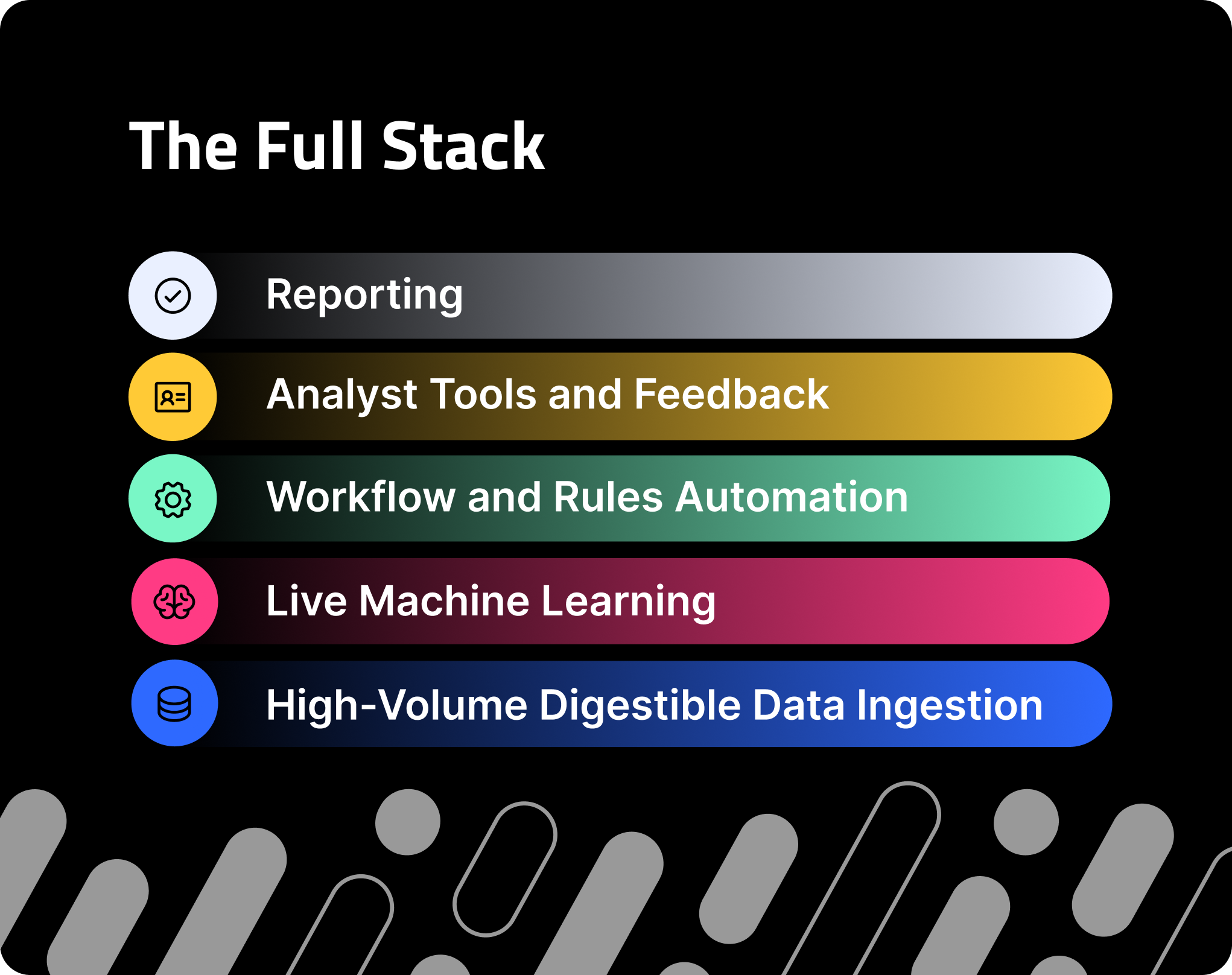

Developing an effective in-house fraud prevention platform is a significant undertaking. It involves multiple layers of technology and expertise. Data ingestion, machine learning models, rules engines, analyst tools, and reporting dashboards all need to work in concert.

Each layer of this stack requires specialized talent. You need data engineers to capture and normalize high-volume event data, data scientists to develop and train machine learning models, fraud analysts to write rules and review edge cases, and infrastructure engineers to ensure uptime, security, and compliance. Even after the initial build, continuous maintenance and updates are essential—fraud patterns change, models need retraining, and new edge cases emerge constantly. All of this amounts to a long-term commitment of time and people.

This is where Total Cost of Ownership (TCO) becomes critical. Building may appear cost-effective on the surface, but the true TCO includes:

- Initial development costs (engineering time, infrastructure, tooling)

- Hiring or reallocating specialized talent (data science, fraud analysis, DevOps)

- Ongoing maintenance and upgrades to adapt to new fraud vectors

- Downtime risks and revenue losses during system errors or model drift

- Compliance and data governance requirements that scale with customer growth

Beyond the visible costs, the opportunity cost is significant. Talent devoted to fraud tooling is talent not building features that differentiate your core product. And if the system underperforms or lacks agility, the downstream costs of false positives, chargebacks, and churn can dwarf your initial savings.

Crucially, an in-house product must keep up with growth. A system that works during early stages might struggle to scale as transaction volumes surge. A homegrown tool might not stop fraud effectively without causing too much friction for good customers. In-house rules can become too strict or even crash under high load, leading to false declines and lost business during critical moments. These challenges mean any company attempting to “go it alone” in fraud prevention needs to be ready for a continual, resource-intensive battle with a high and often underestimated total cost.

If and when risk teams realize they don’t have enough manpower or bandwidth to build a robust fraud tool internally, allocating limited engineering resources to a multi-year build presents an even tougher challenge. The clear alternative in these situations becomes partnering with a dedicated fraud prevention provider.

Advantages of Leveraging a Purpose-Built Solution

Buying a third-party fraud prevention solution like Sift can accelerate a company’s ability to fight fraud. Third-party providers offer ready-made expertise and technology that would take multiple cycles for most companies to replicate. Sift Payment Protection, for example, comes with battle-tested machine learning models and an unrivaled data network processing trillions of global events.

One major advantage of a solution like Sift is that network effect of data. Sift works with hundreds of customers across many industries, feeding its machine learning with a massive breadth of fraud patterns. This global pool of fraud data creates a network intelligence that individual companies simply cannot attain alone. The collective data from Sift’s customer network provides shared intelligence that protects the community.

Additionally, third-party providers bring experience and focus. Fighting fraud is their core business, so they invest heavily in keeping their tools effective. Sift, for instance, processes on the order of one trillion events per year across its customers – a scale that ensures its machine learning models are exposed to an enormous variety of fraud scenarios. The models are constantly updated by a team of experts dedicated solely to fraud prevention. For a customer, this means getting a solution that is continuously improving and able to address new threats, without having to invest your own engineering hours into those improvements.

There are also practical time and efficiency gains. Integration of a cloud-based fraud API can be done in weeks, not years. One Sift customer saw significant, impactful results quickly. Partnering with Sift enabled them to prevent thousands of dollars of fraud a day and made their risk team 2–3x more efficient at reviewing cases. In other words, buying allowed them to save money and time right away.

The scalability of Sift’s platform also meant they could grow without outstripping their fraud defenses—the system handled surges in volume and new fraud patterns seamlessly. Instead of constantly playing catch-up, the team could focus on optimizing strategies and policies (e.g., via Sift’s Console and analytics) rather than firefighting basic fraud detection.

Finally, outsourcing fraud prevention can free your company to focus on its core mission. As one fraud solution provider put it, building in-house gives total control, but buying gives you “the freedom to focus on business operations and growth.” For a fast-scaling software company, handing off the heavy lifting of fraud detection to a trusted partner like Sift can be a strategic move that lets your product and engineering teams concentrate on what differentiates your business, while still maintaining world-class fraud protection.

Of course, even the best purpose-built solution requires a close, collaborative partnership to perform at its highest level. Your fraud prevention platform is only as good as the signals it ingests and the understanding it has of your business. That means working closely with your vendor—providing feedback, sharing contextual signals, and offering relevant data to help optimize the models for your specific environment. By bringing your unique processes and fraud nuances into the model training loop, you enable the system to get smarter, faster. This feedback loop is critical in adapting the solution to your specific risk profile and user behaviors. A proactive, two-way relationship ensures the platform evolves with your needs and keeps pace with the shifting threat landscape.

Choosing the Right Path for Payment Protection

Payment fraud prevention is a mission-critical function that demands both strategic foresight and technical excellence. Deciding whether to build an in-house solution or buy from a specialist like Sift is ultimately about aligning with your company’s goals, capabilities, and appetite for innovation. There is no one-size-fits-all answer, but there are clear patterns.

Building in-house can make sense if fraud prevention is a core differentiator for you, and if you have unique requirements or the resources to invest in a long-term, ever-evolving project. It offers full control, but also full responsibility. For most growth-stage software companies, however, the buy model offers compelling advantages. It provides immediate access to world-class technology and expertise, faster deployment, and the ability to keep fraud-fighting measures at parity with the sophisticated tactics of fraudsters.

As businesses weigh this decision, consider the Total Cost of Ownership, including the hidden costs of missed fraud, opportunity costs of diverted resources, and the long-term burden of maintaining agility and innovation in-house. A well-chosen fraud prevention strategy will pay dividends by not only preventing financial losses but also by enabling your business to grow confidently, knowing that both fraud risks and customer experience are in good hands.

In the fight against online payment fraud, innovation and agility are non-negotiable. Companies need to stay one step ahead of the bad actors, and whether they build or buy, the goal is the same: protect customers and revenue, deliver delightful experiences, and do so in a way that supports sustainable, frictionless growth.